Project Cost Management Processes: Everything You Need to Know

Effective project cost management is vital for success, but keeping costs in check is often easier said than done.

An analysis of almost 1,500 projects revealed that 27% had overruns. Over 15% of projects will have a 200% cost overrun and suffer miserably.

These failures often stem from poor planning, inaccurate cost estimates, and a lack of ongoing cost monitoring. Without a structured approach to resource planning and financial management, projects can easily spiral out of control, leading to delays and cost overruns that affect project outcomes and stakeholder satisfaction.

To avoid these common pitfalls, you need to master the four key processes of cost management: resource planning, cost estimation, cost budgeting, and cost control. These processes ensure that projects stay on track and within budget, delivering the expected results without unnecessary financial surprises.

What Is Project Cost Management?

Project cost management is the process of estimating, budgeting, and controlling costs to ensure that a project is completed within the approved budget.

Project cost management involves systematic steps that help you plan financial resources and monitor spending throughout the project lifecycle. The main goal of project cost management is to minimize financial risk and deliver the project’s expected outcomes without exceeding the allocated funds.

Effective cost management is more than just setting a budget. It encompasses the entire financial planning and execution process, ensuring that every resource is accounted for, expenditures are tracked, and adjustments are made when necessary. Without solid cost management, even the most well-planned projects can face significant financial challenges, leading to delays, scope reduction, or complete failure.

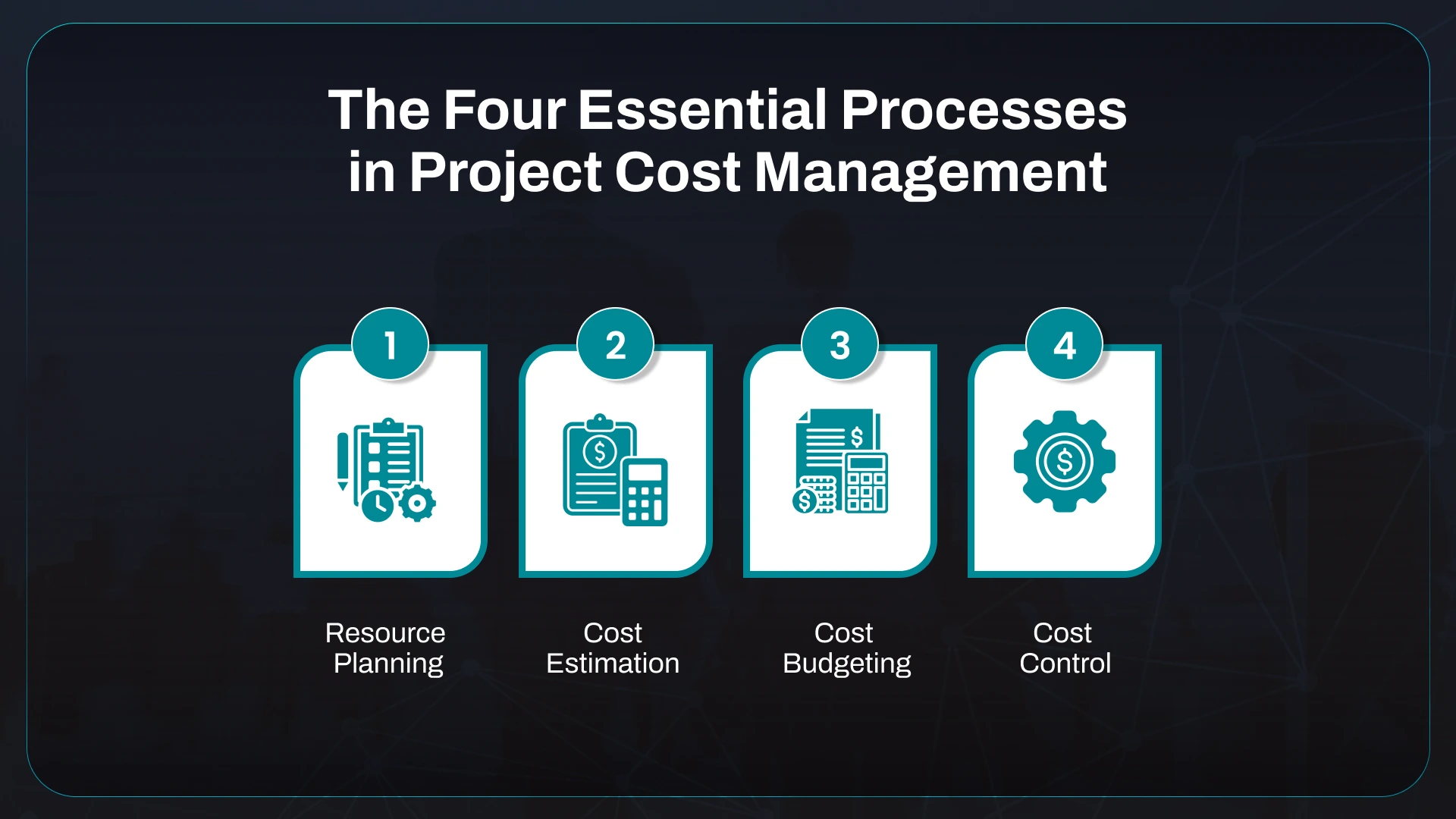

The Four Essential Processes in Project Cost Management

Project cost management involves four critical processes that ensure every financial aspect of a project is carefully planned and monitored. These processes guide how resources are allocated, how much a project will cost, and how to maintain control over spending throughout its lifecycle.

1. Resource Planning

Resource planning is the first essential step in project cost management. This process involves identifying, organizing, and allocating all resources necessary to complete a project. Resources can include human resources, materials, equipment, and other assets required to execute project tasks effectively.

Essential activities in resource planning include

- Identifying Resource Needs: Understanding the specific types and quantities of resources required for each project phase. This includes determining skill sets needed for team members, equipment availability, and material sourcing.

- Allocating Resources: Assigning the identified resources to specific tasks while considering their availability and skill sets. This ensures that the right resources are in place at the right time, helping to prevent delays and inefficiencies.

- Balancing Resources: Ensuring efficient resource allocation does not lead to overworking individuals or underutilizing assets. A balanced approach enhances productivity and morale among team members.

Effective resource planning directly impacts project costs. When resources are efficiently planned and utilized, projects are less likely to incur unexpected expenses due to delays or misallocation. Additionally, this process gives you a clearer picture of the overall budget, making it easier to estimate costs accurately.

2. Cost Estimation

Cost estimation is an essential process in project cost management, as it involves predicting the financial resources needed for each project activity. Accurate cost estimates help you set realistic budgets and ensure adequate funding is available throughout the project lifecycle. Poor forecasts can lead to financial shortfalls, project delays, or failures.

Types of Cost Estimation Techniques

Different techniques can be used for cost estimation, each suitable for varying project complexities and stages.

| Estimation Technique | Description | When To Use | Pros | Cons |

| Analogous Estimation | Uses historical data from similar projects to estimate costs | Early project stages | Quick and easy | Less accurate for unique projects |

| Parametric Estimation | Applies statistical relationships to project variables to estimate costs | When reliable data is available | More accurate for measurable tasks | Requires detailed data |

| Bottom-Up Estimation | Breaks down individual tasks and sums their costs | For complex projects | Highly accurate | Time-consuming |

Critical Steps in Cost Estimation

- Gather Data: Collect historical data, expert opinions, and market research relevant to the project. Analyzing past project costs can provide valuable insights and help avoid pitfalls experienced in previous endeavors. Engaging with subject matter experts offers practical perspectives, while market research ensures that estimates reflect current pricing trends and resource availability.

- Select Estimation Technique: Choose the appropriate technique based on project complexity and available data. Different approaches, such as analogous estimating for quick approximations or bottom-up estimating for detailed analyses, can yield varying levels of accuracy. Selecting the proper method is crucial to ensuring that estimates are realistic and achievable.

- Calculate Estimates: Use the chosen technique to derive cost estimates for each project activity. This process involves inputting the gathered data into the selected estimation method and generating a comprehensive cost breakdown. Accurate calculations at this stage are essential to create a realistic budget that guides project execution.

- Review and Refine: Validate estimates through peer reviews and adjust based on feedback. Involving team members in the review process enhances the credibility of estimates and can identify potential oversights. By incorporating feedback, you can refine your estimates, leading to a more reliable and actionable budget.

Practical estimation also involves continuous monitoring and adjustments throughout the project. Revisiting estimates as project conditions change ensures the budget remains aligned with actual spending.

3. Cost Budgeting

Cost budgeting aggregates the estimated costs of individual project activities to establish an overall budget. This budget serves as a financial blueprint, guiding you in allocating funds, monitoring expenses, and ensuring that the project remains on track financially. An effective budgeting process is essential for managing cash flow and preventing financial overruns.

Essential Steps in Cost Budgeting

- Develop a Budget Baseline: Combine cost estimates into a comprehensive budget. This comprehensive budget is the benchmark for measuring financial performance throughout the project. By establishing a baseline, you can track actual expenditures against planned costs, allowing for early identification of variances and enabling corrective actions when necessary.

- Allocate Budget to Activities: Distribute the budget across various project tasks and phases, ensuring that resources are available when needed. Thoughtful allocation helps prioritize critical activities and ensures that each task is adequately funded to meet its objectives. This step is crucial for maintaining project momentum and minimizing delays caused by funding shortages.

- Establish Contingency Reserves: Set aside funds for unforeseen expenses. A common practice is to allocate a percentage of the total budget—often ranging from 5% to 15%—to handle potential risks and uncertainties. By planning for contingencies, you can mitigate the impact of unexpected challenges without derailing the project.

- Create a Schedule for Spending: Develop a timeline for when funds will be needed. This timeline helps manage cash flow effectively, ensuring resources are available for critical tasks when required. By scheduling expenditures, you can avoid financial bottlenecks and ensure smooth project progression, ultimately leading to successful project delivery.

Budget Monitoring Table:

A monitoring table can be helpful in effectively tracking the project budget. Here’s a sample budget monitoring table format:

| Project Activity | Estimated Cost | Actual Cost | Variance | Notes |

| Activity 1 | $10,000 | $9,500 | -$500 | Under budget |

| Activity 2 | $15,000 | $16,500 | +$1,500 | Delays led to extra cost |

| Activity 3 | $5,000 | $5,000 | $0 | On track |

4. Cost Control

Cost control is monitoring and managing project costs to ensure expenditures remain within the approved budget. This ongoing activity is crucial throughout the project lifecycle, as it allows you to identify variances between estimated and actual costs and make necessary adjustments to keep the project financially viable.

Essential Steps in Cost Control

- Monitor Project Costs: Regularly compare actual spending against the budget baseline. This ongoing monitoring allows you to identify discrepancies early on, enabling them to take corrective action before minor issues escalate into significant financial problems. By consistently tracking costs, teams can maintain control over project finances and ensure that expenditures align with budgetary expectations.

- Analyze Variances: Investigate significant variances to determine their causes. Understanding why costs deviate from the plan is crucial for effective management. For instance, a variance may arise due to unexpected labor costs or price increases in materials. Analyzing these variances allows you to implement targeted corrective actions, improving future budget accuracy and project control.

- Implement Corrective Actions: Based on variance analysis, make informed decisions to address issues. This may involve reallocating resources to critical areas, adjusting the project scope to accommodate financial realities, or revisiting cost estimates to better align with actual conditions. Taking proactive steps ensures that the project remains on track financially and meets its objectives despite challenges.

- Communicate with Stakeholders: Keep all stakeholders informed about financial performance and any necessary changes. Clear communication fosters trust and ensures everyone is aligned with the project’s financial goals. Regular updates and transparent discussions about budget status and variances help maintain stakeholder confidence and engagement throughout the project lifecycle.

Cost Control Techniques:

Several techniques can enhance cost control effectiveness, including:

| Technique | Description | Benefits |

| Earned Value Management | Compares the planned progress with actual progress in terms of cost and schedule | Provides a comprehensive view of project performance |

| Cost Performance Index (CPI) | Measures cost efficiency by comparing earned value to actual costs | Helps check financial health |

| Change Control Process | Manages changes to project scope, budget, or schedule to minimize financial impact | Reduces risk of budget overruns |

Also Read: The Ultimate Guide to Earned Value Management

Effective cost control keeps the project within budget and contributes to overall success. It improves the team’s ability to deliver quality results while maintaining financial accountability.

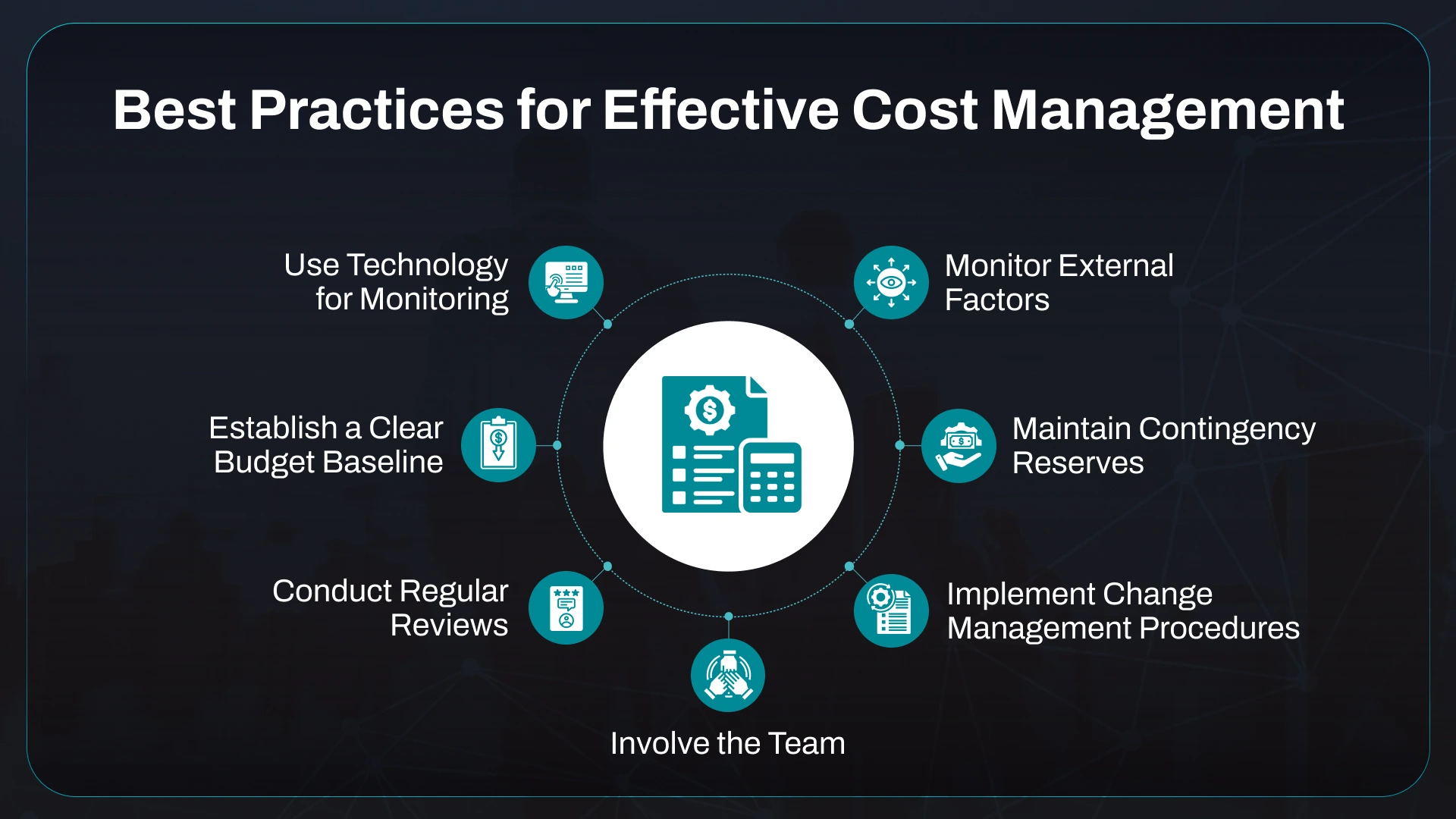

Best Practices for Effective Cost Management

Here are some effective strategies to consider for effective project cost management:

- Establish a Clear Budget Baseline: Before beginning a project, create a detailed budget outlining all estimated costs. This baseline should be approved by key stakeholders and used as a reference point throughout the project. A well-defined baseline allows for better tracking of financial performance and helps identify variances.

- Use Technology for Monitoring: Project management software offers budgeting and cost-tracking features. Tools like Microsoft Project, Asana, or specialized financial software can provide real-time insights into spending, helping managers make informed decisions quickly.

- Conduct Regular Reviews: Schedule frequent budget reviews to compare actual spending against the planned budget. These reviews can help identify spending trends, allowing you to adjust plans proactively rather than reactively.

- Involve the Team: Engage team members in the budgeting and cost management processes. Their insights can lead to more accurate estimates and help identify potential cost-saving measures. Fostering a culture of financial accountability also encourages everyone to be mindful of spending.

- Implement Change Management Procedures: Establish a formal change management process for project scope changes. This process should include thoroughly assessing how changes affect the budget, and ensuring adjustments are carefully considered and documented.

- Maintain Contingency Reserves: Allocate a portion of the budget for unexpected expenses. This reserve provides a financial cushion and the flexibility to address unforeseen challenges without derailing the entire project.

- Monitor External Factors: Stay aware of external factors that may impact costs, such as market conditions, supplier pricing, and economic trends. Adjusting project plans in response to these factors can help mitigate potential budget risks.

Maximize Your Project Potential with Probodata’s evData Pro!

Effective project cost management is essential for ensuring your projects are delivered on time and within budget. By mastering the processes of resource planning, cost estimation, cost budgeting, and cost control, you can enhance your project’s financial performance and reduce the risk of overruns. However, implementing these practices requires the right tools and support.

At Probodata, we understand project managers’ challenges and offer tailored solutions to simplify project cost management. Our tool, evData Pro, is an add-on to Deltek Cobra, and provides excellent data analytics and project tracking capabilities that empower you to make informed financial decisions.

With features designed for real-time cost monitoring, budget forecasting, and comprehensive reporting, evData Pro enables you to control your project finances effortlessly.

Additionally, our services include:

- Data Integration: Seamlessly integrate project data from Deltek Cobra and scheduling software to have a unified view of your financial performance.

- Customized Reporting: Generate reports that cater to your project’s needs, helping you quickly identify trends and variances.

- Consulting Services: Work with our experts to develop strategies tailored to your organization’s unique project management challenges.

Don’t let financial mismanagement hinder your project’s success. Explore how Probodata’s evData Pro can transform your project cost management.

Contact Us Today!